Using our assessment of fees, portfolio construction, and automation features, the best robo advisors in Australia in 2026 are Spaceship Voyager (best for beginners), Stockspot (best for automated ETF portfolios), InvestSMART (best for capped-fee portfolios), Raiz Invest (best for micro-investing), and QuietGrowth (best for long-term managed portfolios with formal advice).

These platforms offer automated portfolio management using diversified ETFs, operate under Australian regulatory frameworks, and allow investors to build portfolios with minimal manual management.

Top Australian robo advisors by category

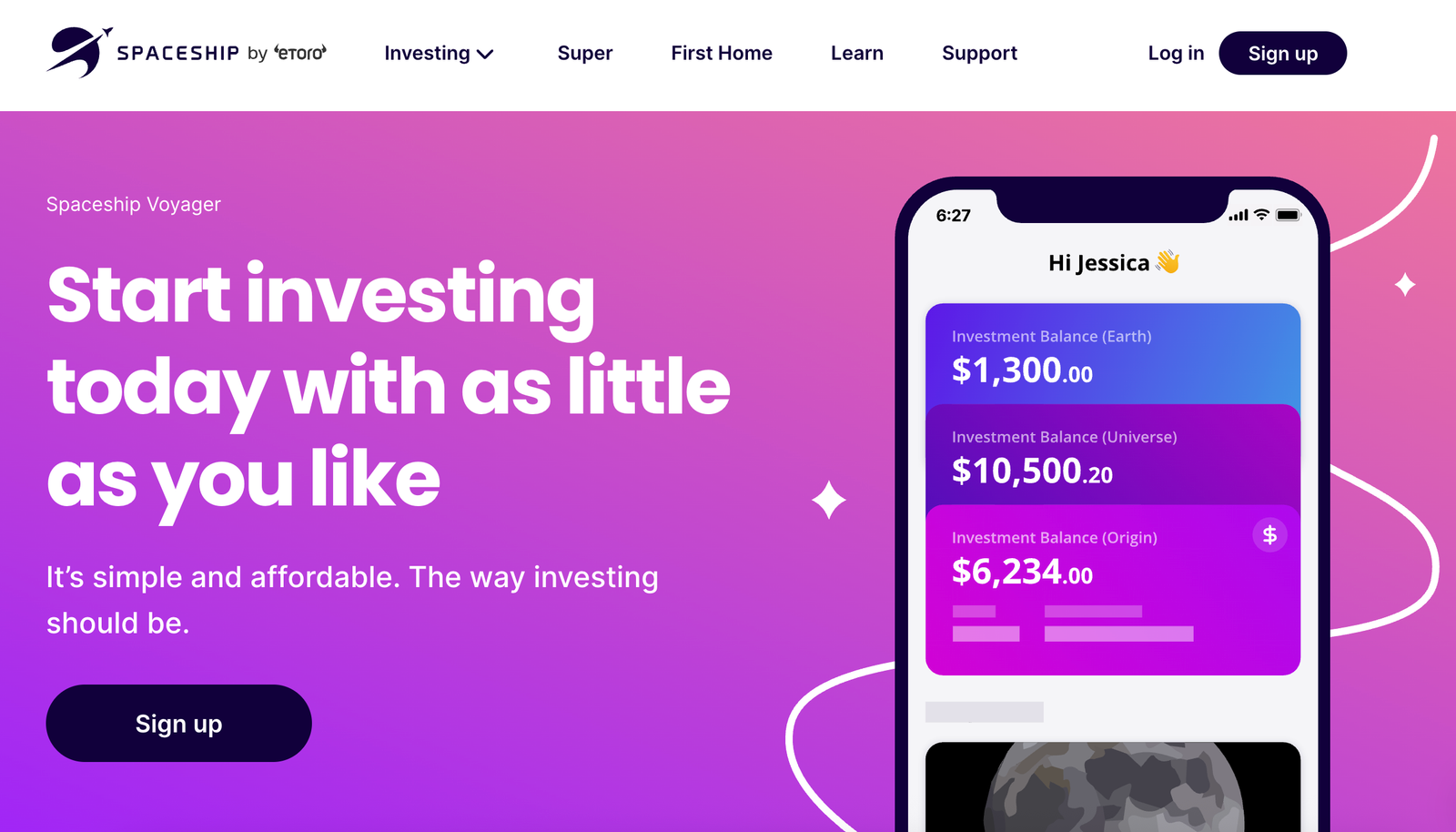

- Best for First-Time Investors: Spaceship Voyager by eToro offers simple app-based investing with no minimum investment, making it one of the easiest entry points for Australians starting their first portfolio.

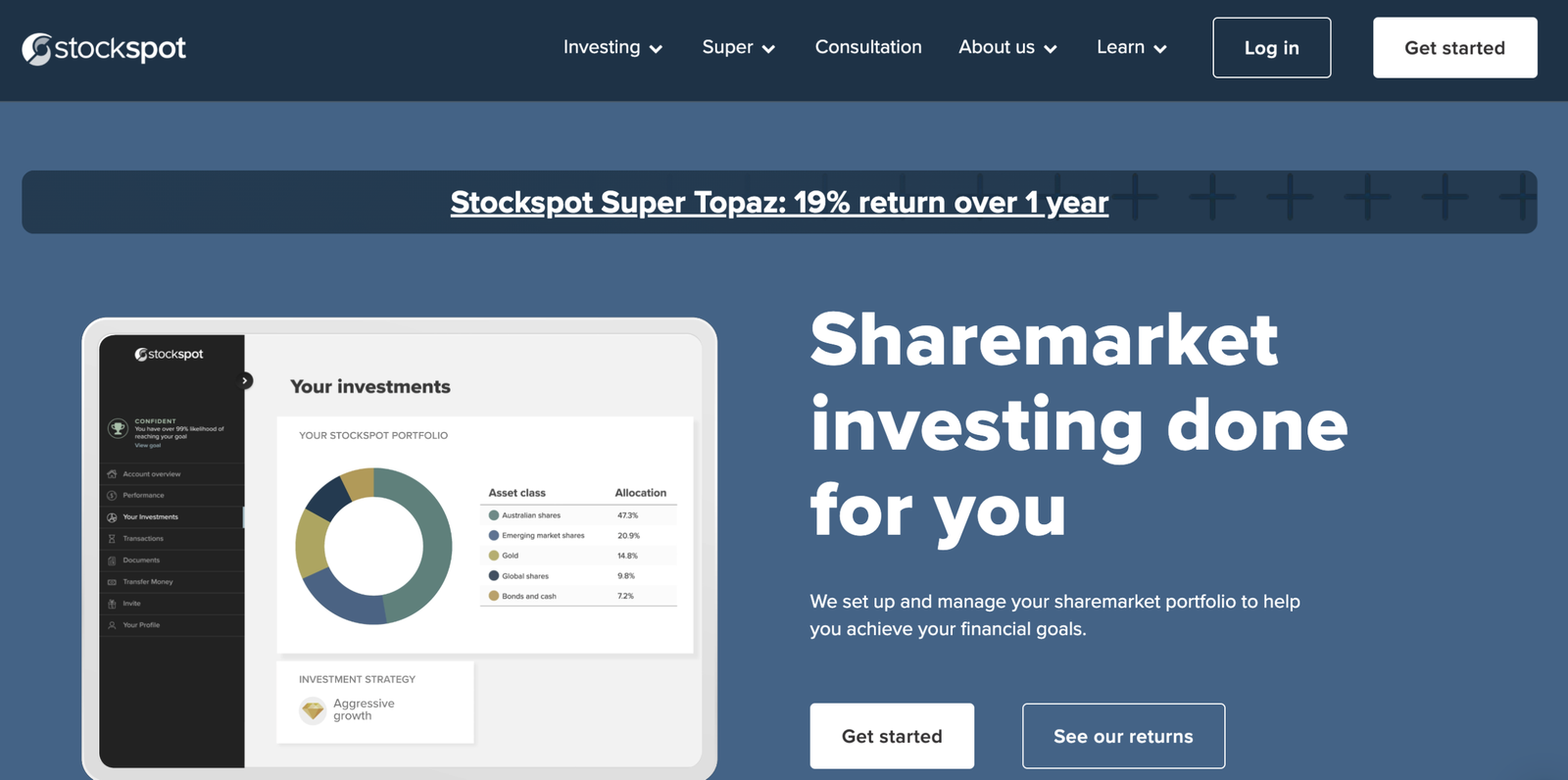

- Best for Fully Automated ETF Portfolios: Stockspot is a long-established robo advisor offering disciplined, diversified ETF portfolios with automated rebalancing and a strong track record in the Australian market.

- Best for Capped Fees on Larger Portfolios: InvestSMART provides professionally managed portfolios with a capped management fee, which can make it attractive for investors managing mid-to-large balances.

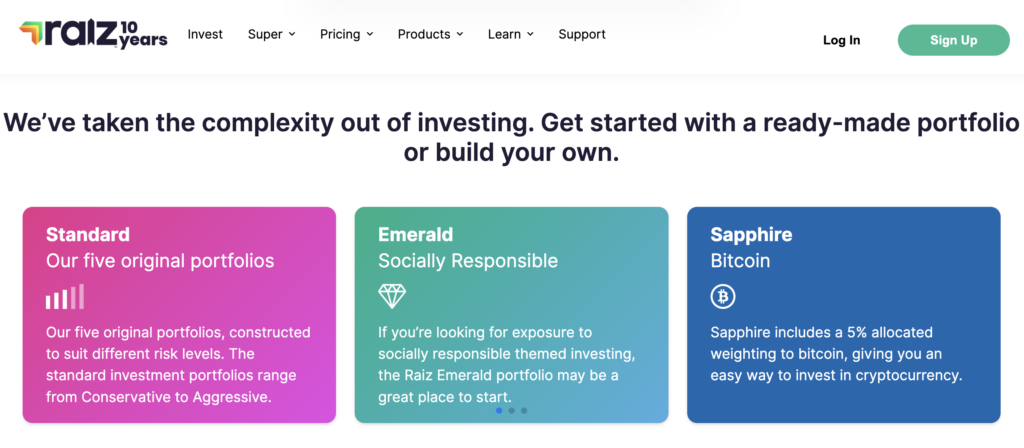

- Best for Micro-Investing: Raiz Invest allows investors to automatically invest spare change from everyday purchases, making it popular for users starting with very small balances.

- Best for Long-Term Managed Advice: QuietGrowth provides MDA-based robo advice with HIN ownership and Statements of Advice, appealing to investors who want structured long-term portfolio management.

Key considerations when choosing a Robo Advisor

- Fees: Most robo advisors charge either a percentage of assets under management (AUM) or a flat monthly fee depending on the platform and portfolio size.

- Minimum Investment: Minimum deposits vary widely. Some platforms like Spaceship and Raiz allow very small starting balances, while others may require higher initial investments.

- Portfolio Construction: Most Australian robo advisors invest primarily in diversified ETF portfolios designed to spread risk across global equities, bonds, and other asset classes.

- Automation and Rebalancing: Robo advisors automatically rebalance portfolios and manage allocations, helping investors stay aligned with their long-term strategy without manual trading.

What are the best robo advisors in Australia in 2026?

| Platform | Structure | Minimum Investment | Fees (Platform Only) | Best For |

|---|---|---|---|---|

| Spaceship Voyager | Managed Investment Scheme (pooled unit trust) | $0 | $3/month + 0.15%–0.50% p.a. | First-time investors wanting simple, app-based growth portfolios with no minimum investment |

| Stockspot | Managed Investment Scheme (custodian held ETFs) | $2,000 | $1/month under $20k; 0.396%–0.66% p.a. above | Hands-off investors wanting automated, diversified ETF portfolios with scale and long track record |

| InvestSMART | Professionally Managed Account (beneficial ownership retained) | $5,000 | 0.44% p.a. to $200k; capped at $880 p.a. above + 0.11% admin | Mid-to-large portfolios seeking capped fees and professionally managed accounts |

| Raiz Invest | Managed Investment Scheme (pooled fund) | $5 | $2.50–$6.50 per month or 0.275% p.a. (tiered) | Micro-investors who want round-up investing and a low minimum starting balance |

| QuietGrowth | Managed Discretionary Account (HIN structure) | $3,000 | 0.36%–0.60% p.a. tiered | Long-term investors wanting MDA robo advice with HIN ownership and formal Statements of Advice |

Robo advisor Australia reviews

These robo advisor Australia reviews break down the top platforms based on fees, portfolio strategy, automation features, and which services suit different types of investors.

1. Spaceship Voyager by eToro – Best for beginner investors wanting a simple, low-minimum robo advisor

Platform overview

| Feature | Details |

|---|---|

| Founded | 2017 |

| Clients | 200,000+ across Spaceship platform (est.) |

| Assets Under Management | Multi-billion across Spaceship group |

| Regulation | ASIC regulated managed investment schemes |

| Portfolio Options | 5 (Universe, Earth, Origin, Galaxy, Explorer) |

| Minimum Investment | $0 |

| Fees | $3/month (≥$100 balance) + 0.15%–0.50% p.a. |

| Brokerage | $0 |

| Rebalancing | Managed internally by fund managers |

| Sustainable Options | Yes (Earth Portfolio) |

| Super Option | Yes (separate Spaceship Super product) |

Is Spaceship Voyager regulated in Australia and how is your money protected?

Yes. Spaceship Voyager portfolios operate as registered managed investment schemes regulated by ASIC. Your money is pooled with other investors in a unit trust structure, and you receive units representing your proportional ownership.

It does not provide personal financial advice. You choose the portfolio yourself. A related entity, Spaceship Financial Services Pty Ltd, was fined by ASIC in 2018 for misleading conduct, which is worth noting from a governance perspective. Capital is not guaranteed.

What are the total annual fees and underlying investment costs?

Fees are simple and relatively low.

- $3 per month if your balance is $100 or more

- $0 per month under $100

- Management fees:

- Universe: 0.50% p.a.

- Earth: 0.50% p.a.

- Galaxy: 0.35% p.a.

- Explorer: 0.25% p.a.

- Origin (index): 0.15% p.a.

- No contribution, withdrawal or brokerage fees

For small balances, the flat $3 monthly fee can have a noticeable impact. At higher balances, total costs are competitive relative to active managed funds as the 3$ per month becomes far less significant.

How are portfolios constructed, diversified, and rebalanced?

Spaceship offers five portfolios ranging from conservative (Explorer) to high growth (Universe, Earth, Origin).

- Universe: Actively selected global growth companies

- Earth: Impact-focused equities aligned with sustainability themes

- Origin: Equal-weighted index of 200 global and Australian companies

- Galaxy: Balanced growth and defensive mix

- Explorer: Defensive tilt with bonds and cash

Portfolios invest directly in shares and some ETFs. Technology exposure is significant in growth options. There is no gold allocation and no currency hedging. As a unit trust, rebalancing decisions are made internally by the fund manager.

1-year returns to 31 Dec 2025:

- Universe: 9.3%

- Earth: 10.0%

- Origin: 10.0%

- Galaxy: 5.5%

- Explorer: 3.8%

Past performance is not a guarantee of future results.

What is the minimum investment and how flexible is the account?

There is no minimum investment, which is one of Spaceship’s biggest advantages. You can:

- Set up weekly, fortnightly or monthly auto-investments

- Withdraw anytime with no exit fees

- Hold multiple portfolios and still pay one monthly fee

It is designed for micro-investing and gradual wealth building.

What tools, reporting, and support features are included?

Spaceship is fully app-based. Features include:

- Real-time portfolio tracking

- Holdings transparency

- Curated investment news

- Automated recurring deposits

There is no personalised advice and no adviser team. Customer support is digital-first.

Who is this robo advisor best for?

Spaceship Voyager suits younger investors or beginners who want to invest small amounts with minimal friction. The zero minimum and automated deposits make it accessible.

It is less suitable for investors seeking personalised advice, deep diversification beyond growth equities, or large-balance fee optimisation.

Read the complete eToro review here.

Pros and cons

- No minimum investment

- Low percentage fees

- Simple app-based investing

- No brokerage or exit fees

- No personalised advice

- Flat $3 monthly fee impacts small balances

- Growth portfolios heavily tech-weighted

- Pooled unit trust structure

2. StockSpot – Best for hands-off investors who want automated ETF portfolios

Platform overview

| Feature | Details |

|---|---|

| Founded | 2013 |

| Clients | 16,000+ |

| Assets Under Management | $1 billion+ |

| Regulation | AFSL 536082, regulated by ASIC |

| Portfolio Options | 7 diversified ETF portfolios |

| Minimum Investment | $2,000 standard accounts |

| Fees | $1/month under $20k, 0.396%–0.66% p.a. above $20k |

| Brokerage | $0 |

| Rebalancing | Automatic |

| Sustainable Options | Yes |

| Super Option | Yes, including SMSF |

Is Stockspot robo advisor regulated in Australia and how is your money protected?

Yes. Stockspot operates under AFSL 536082 and is regulated by ASIC. Client assets are held via a third-party custodian and ETFs are structured so holdings remain separate from the company’s balance sheet.

Founded in 2013, it manages over $1 billion for 16,000+ clients, making it one of Australia’s more established robo advisers.

What are the total annual fees and underlying investment costs?

Fees are straightforward but not ultra-cheap.

- Under $20,000: $1 per month

- Over $20,000: 0.396%–0.66% p.a.

- Brokerage: $0

Underlying ETF costs average around 0.27% p.a., meaning total costs for a $20k account can approach ~0.9% p.a.

This is a premium over DIY ETF investing, so the value lies in automation and discipline rather than cost leadership.

How are portfolios constructed, diversified, and rebalanced?

Stockspot uses diversified ETF portfolios spanning Australian and global equities, emerging markets, fixed income, gold, and cash.

There are seven portfolios ranging from Conservative (Amethyst) to Aggressive Growth (Topaz), plus sustainable options. Rebalancing, dividend reinvestment, and tax loss harvesting are automated, helping reduce emotional decision-making.

What is the minimum investment and how flexible is the account?

The minimum investment is $2,000. Accounts are available for individuals, joint investors, kids, trusts, companies, and SMSFs.

There are no lock-in periods. Investors can add or withdraw funds, subject to ETF settlement timeframes.

What tools, reporting, and support features are included?

Clients receive performance tracking, asset allocation breakdowns, and tax reporting summaries. Deposits are auto-invested and portfolios are automatically rebalanced.

An Australian-based support team is available, though it is not a replacement for full financial planning advice.

Who is Stockspot best for?

Stockspot suits investors who want hands-off, diversified ETF exposure with behavioural guardrails. It is best for busy professionals who value automation.

Fee-sensitive DIY investors comfortable managing their own ETF portfolio may find it expensive relative to self-directed investing.

Pros and cons

- ASIC regulated, established since 2013

- Automated rebalancing and tax features

- $1bn+ under management

- Sustainable and super options

- Higher cost than DIY ETF investing

- Limited personalisation

- Not full financial planning

3. InvestSMART – Best for mid-to-large investors wanting capped fees and active oversight

Platform overview

| Feature | Details |

|---|---|

| Founded | 1999 (robo service launched 2015) |

| Clients | ~3,400 PMA clients (Dec 2025) |

| Assets Under Management | $750m+ (Dec 2025) |

| Regulation | ASIC regulated, AFSL holder |

| Portfolio Options | 5 diversified + single asset portfolios |

| Minimum Investment | $5,000 |

| Fees | 0.44% p.a. to $200k, capped at $880 p.a. above + 0.11% admin |

| Brokerage | Sell trades: greater of $4.40 or 0.044% |

| Rebalancing | Active management with periodic rebalancing |

| Sustainable Options | Ethical Growth portfolio available |

| Super Option | SMSF accounts supported |

Is InvestSMART regulated in Australia and how is your money protected?

Yes. InvestSMART operates under an Australian Financial Services Licence and is regulated by ASIC. Investments are held via a Professionally Managed Account (PMA) structure, meaning you retain beneficial ownership of the underlying holdings rather than being pooled in a traditional managed fund.

The business has been operating since 1999 and manages over $750 million as at December 2025. That longevity adds credibility, though as with all market investments, capital is not guaranteed.

What are the total annual fees and underlying investment costs on InvestSMART?

InvestSMART uses a capped fee model that becomes competitive at larger balances.

- 0.44% p.a. up to $200,000

- $880 per year cap above $200,000

- 0.11% p.a. admin fee

- Sell brokerage: greater of $4.40 or 0.044%

- ETF indirect costs: typically 0.09%–0.30% p.a.

For mid-sized balances, total ongoing costs usually sit around 0.6%–0.8% plus ETF fees. It is cheaper than many active managed funds but not as low as pure DIY ETF investing.

How are portfolios constructed, diversified, and rebalanced?

InvestSMART offers five diversified portfolios: Conservative, Balanced, Growth, High Growth and Ethical Growth. Asset classes include Australian equities, global equities, fixed income, property and cash.

Portfolios are actively managed and regularly rebalanced. Built-in tax efficiency, including tax-aware rebalancing, is part of the system.

Performance to 31 December 2025:

1 year

- Conservative: +5.3%

- Balanced: +6.9%

- Growth: +8.7%

- High Growth: +10.2%

3 years p.a.

- Growth: +11.5%

- High Growth: +14.3%

Returns are after fees but, as always, past performance does not guarantee future results.

What is the minimum investment and how flexible is the account?

The minimum investment is $5,000, which is higher than some competitors.

Account options include individual, joint, trustee for child, and SMSF accounts. There are no withdrawal or switching fees. Regular contribution plans can be set up via direct debit. Unlike some robo advisers, there is no fee-free micro-investing tier.

What tools, reporting, and support features are included?

InvestSMART provides:

- Online portfolio dashboard

- Performance reporting

- Tax summaries

- Market insights and calculators

- Mobile app access

The robo algorithm matches you to a portfolio based on risk profiling. However, there is no dedicated financial adviser team. Support is provided via a contact centre rather than personalised advice.

Who is InvestSMART best for?

InvestSMART suits investors with $5,000+ who want professionally managed, diversified portfolios without paying traditional adviser fees. The capped fee model becomes particularly attractive at higher balances.

It is less suitable for beginners with very small starting amounts or investors seeking deep customisation or holistic financial planning.

Pros and cons

- ASIC regulated with AFSL and long track record (since 1999)

- Capped fee structure becomes very cost-effective for larger portfolios

- Professionally Managed Account (PMA) means you retain beneficial ownership

- No exit or switching fees and flexible account options (including SMSF)

- $5,000 minimum investment is higher than many robo advisors

- Limited personal advice, no dedicated financial adviser support

4. Raiz Invest – Best for micro-investors wanting round-up, set-and-forget investing

Platform overview

| Feature | Details |

|---|---|

| Founded | 2016 (formerly Acorns Australia) |

| Clients | 268,000+ Australians; 1.6m+ globally |

| Assets Under Management | Multi-billion across group (est.) |

| Regulation | ASIC regulated Managed Investment Scheme |

| Portfolio Options | 8 portfolios (incl. ESG, Bitcoin, Property, Plus custom) |

| Minimum Investment | $5 |

| Fees | $2.50–$6.50 per month or 0.275% p.a. (tiered) |

| Brokerage | $0 (included in account fee) |

| Rebalancing | Automatic |

| Sustainable Options | Yes (Emerald portfolio) |

| Super Option | No direct super fund |

Is Raiz robo advisor regulated in Australia and how is your money protected?

Yes. Raiz operates as an ASIC-regulated managed investment scheme. Instreet Investment Limited acts as Responsible Entity and Australian Executor Trustees is the Trustee. Your funds are pooled with other investors and held via a custodian structure.

It does not provide a personal Statement of Advice. Investors choose portfolios themselves. As with any managed fund, there is custodian and market risk, and capital is not guaranteed.

What are the total annual fees and underlying investment costs

Raiz uses a tiered flat-fee model that can be expensive for small balances.

- Lite: $2.50 per month (limited portfolios)

- Regular: $5.50 per month under $26k, then 0.275% p.a. above

- Plus: $6.50 per month under $28k, then 0.275% p.a. above

- Sapphire and Property portfolios: $5.50/month + 0.275% p.a.

Underlying ETF management costs apply separately. There are no brokerage, deposit or withdrawal fees.

For balances under $1,000, the flat monthly fee can equate to several percent per year. At higher balances, the percentage fee becomes more competitive.

How are portfolios constructed, diversified, and rebalanced?

Raiz offers eight portfolios ranging from Conservative to Aggressive, plus Emerald (ESG), Sapphire (includes 5% Bitcoin), Property and Plus (customisable).

Portfolios are primarily built using ASX-listed ETFs, inspired by modern portfolio theory associated with Dr Harry Markowitz. The Plus portfolio allows selection from ETFs, 50 ASX stocks, Bitcoin or a property fund.

Rebalancing is automatic. Dividends and distributions are reinvested by default.

What is the minimum investment and how flexible is the account?

The minimum investment is $5, making Raiz one of the most accessible robo platforms in Australia.

Investors can:

- Use round-ups from everyday purchases

- Set recurring deposits

- Invest lump sums

- Withdraw at any time with no exit fee

Raiz Kids allows sub-accounts for children under 18 within your main account.

What tools, reporting, and support features are included?

Raiz is app-first. Features include:

- Round-up micro-investing

- Cashback rewards from partner retailers

- Portfolio performance dashboard

- Automatic dividend reinvestment

Customer support is primarily digital. Raiz scored above average for overall satisfaction but slightly below average for trust relative to competitors.

Who is this robo advisor best for?

Raiz suits beginners who want to start investing with very small amounts and automate the process through round-ups. It works well for habitual savers building wealth gradually.

It is less suitable for investors with larger balances seeking the lowest percentage fees or fully personalised portfolio advice.

Pros and cons

- $5 minimum investment

- Round-up micro-investing feature

- Automatic rebalancing

- ESG, Bitcoin and custom portfolio options

- Flat monthly fees can be high for small balances

- No personalised advice

- Pooled managed fund structure

- Underlying ETF fees apply

5. QuietGrowth – Best for long-term investors wanting low-cost MDA robo advice with HIN ownership

Platform overview

| Feature | Details |

|---|---|

| Founded | 2014 (managing client funds since 2015) |

| Clients | Thousands globally (private firm) |

| Assets Under Management | Not publicly disclosed |

| Regulation | ASIC regulated MDA robo adviser (AFSL holder) |

| Portfolio Options | 5 diversified ETF portfolios |

| Minimum Investment | $3,000 |

| Fees | 0.36%–0.60% p.a. (tiered) |

| Brokerage | $0 |

| Rebalancing | Automatic |

| Sustainable Options | No dedicated ESG portfolio |

| Super Option | Yes (SMSF supported) |

Is QuietGrowth robo advisor regulated in Australia and how is your money protected?

Yes. QuietGrowth operates in Australia as an ASIC-regulated Managed Discretionary Account (MDA) robo adviser. It issues a Statement of Advice (SOA) and manages investments on your behalf under an MDA agreement.

Securities are held under your own individual HIN, which means assets are in your name rather than pooled in a unit trust. That structure offers greater transparency compared to many managed fund-based robo platforms.

What are the total annual fees and underlying investment costs?

QuietGrowth uses a declining tiered fee model:

- $3,000–$10,000: 0.60% p.a.

- $10,001–$200,000: 0.50% p.a.

- $200,001–$2m: 0.40% p.a.

- $2m+: 0.36% p.a.

There are no brokerage, platform or exit fees. Underlying ETF management costs apply separately, typically low-cost index ETFs.

For balances under $10,000 it is mid-range on price. For six-figure portfolios, fees become more competitive relative to traditional financial advisers.

How are portfolios constructed, diversified, and rebalanced?

QuietGrowth builds portfolios using 8 ETFs across 6 asset classes:

- Australian shares

- International developed markets

- Emerging markets

- Dividend shares

- Bonds

- Natural resources (including gold exposure)

There are five risk profiles, from conservative (higher bond allocation) to aggressive (90%+ equities). Portfolios are grounded in Modern Portfolio Theory associated with Markowitz and Fama.

Rebalancing is automatic. Tax-loss harvesting is available. Allocation adjustments are driven by algorithmic risk optimisation.

What is the minimum investment and how flexible is the account?

The minimum investment is $3,000, higher than micro-investing apps but lower than many traditional advisers.

Supported account types include:

- Individual

- Joint

- Trust

- Company

- SMSF

Funds can be added or withdrawn, though withdrawals settle according to brokerage timelines. There is no dedicated kids account.

What tools, reporting, and support features are included?

QuietGrowth offers:

- Online dashboard and mobile app

- Risk questionnaire and personalised portfolio

- Statement of Advice

- Goal-based investing options

- SMSF integration via Green Frog Super partnership

Unlike app-only micro platforms, QuietGrowth positions itself as a digital financial adviser rather than a savings app.

Who is this robo advisor best for?

QuietGrowth suits investors with $3,000+ who want structured, long-term ETF investing with an adviser-style framework but without traditional adviser fees.

It is less suitable for micro-investors or those seeking highly customised or thematic portfolios beyond diversified ETF exposure.

Pros and cons

- ASIC-regulated MDA with SOA issued

- Individual HIN structure

- Automatic rebalancing and tax-loss harvesting

- Tiered fees reduce at higher balances

- $3,000 minimum investment

- ETFs only, limited customisation

- No dedicated ESG portfolio

What are robo advisors?

Robo advisors are digital investment platforms that build and manage diversified portfolios for you using algorithms instead of a human stock picker. In Australia, most operate under an AFSL and invest primarily in low-cost ETFs across shares, bonds and sometimes alternatives.

They are not trading apps. You don’t pick individual stocks. Instead, you answer a risk questionnaire, receive a recommended asset allocation, and the platform manages rebalancing and administration on your behalf.

How do robo advisors work?

Robo advisors start with a risk and goals assessment, then assign you to a diversified portfolio aligned to your time horizon and tolerance for volatility. Portfolios are usually built using ETFs covering Australian shares, global equities, fixed income and sometimes gold or property.

Once funded, the platform handles:

- Automatic rebalancing

- Dividend reinvestment

- Ongoing portfolio monitoring

- Tax reporting and sometimes tax-loss harvesting

Some Australian providers operate as Managed Investment Schemes. Others use a Managed Discretionary Account structure where securities sit under your own HIN. The mechanics differ, but the objective is the same: disciplined, rules-based investing.

Are robo advisors worth It?

For many investors, yes. For others, not at all.

If you would otherwise sit in cash, panic during market dips, or never rebalance, a robo advisor can add real behavioural value. Automation removes emotion. That alone can improve long-term outcomes.

If you are comfortable building and maintaining a low-cost ETF portfolio yourself, the additional platform fee may not justify the convenience. The value is not in “beating the market”. It is in structure, discipline and time saved.

What is the average performance of robo advisors?

Robo advisors do not promise to outperform the market. Most track global market returns according to their asset allocation.

Long-term performance generally mirrors:

- Equity market returns for growth portfolios

- A blended equity and bond return for balanced portfolios

- Lower volatility and lower returns for conservative portfolios

Over the past decade, diversified growth portfolios in Australia have often delivered high single-digit to low double-digit annualised returns before tax, depending on market conditions. Returns vary materially year to year. There are no guarantees.

The key driver of performance is asset allocation, not the robo brand.

Robo advisors vs. financial advisors

A robo advisor is structured and automated. A financial adviser is personalised and strategic.

Robo platforms focus on portfolio construction and maintenance. They rarely provide estate planning, tax structuring, insurance advice or retirement modelling beyond basic projections.

A licensed financial adviser can deliver holistic strategy but typically charges materially higher fees, often 0.8% to 1.5% p.a. plus upfront advice costs.

If your needs are straightforward and portfolio-based, robo advice can be sufficient. If you run a business, have complex tax considerations or are approaching retirement, human advice often adds more value.

Pros and cons of robo advisors

- Low minimum investment requirements

- Automated rebalancing

- Diversified ETF exposure

- Lower fees than traditional advisers

- Reduced emotional decision-making

- Limited customisation

- No comprehensive financial planning

- Ongoing platform fees

- Market risk still applies

- You remain responsible for tax outcomes

Robo advisors fees

Australian robo advisor fees typically fall into three categories:

- Platform or management fee – Often 0.25% to 0.60% p.a.

- Underlying ETF fees – Usually 0.05% to 0.30% p.a.

- Flat monthly fees – Common in micro-investing apps

All-in costs for most portfolios land between 0.4% and 0.9% per year, depending on balance size and provider.

Flat monthly fees can be expensive for small balances. Percentage fees become more competitive as account size grows. Always check whether brokerage, administration or transaction costs are included.

How much money can you make with robo advisors?

There is no fixed return.

Your outcome depends on:

- Asset allocation

- Time invested

- Market performance

- Fees

- Behaviour

A high-growth portfolio might average 7% to 10% annually over long periods. A conservative portfolio may average materially less. Short-term losses are normal.

Robo investors are designed for steady, long-term compounding. They are not income-generation tools or shortcuts to fast wealth.

Are robo advisors safe in australia?

Yes, robo advisors are legal and regulated in Australia, but “safe” does not mean risk-free.

Most Australian robo advisors operate under an Australian Financial Services Licence (AFSL) issued by the Australian Securities and Investments Commission (ASIC). This means they must comply with conduct, disclosure, capital adequacy and client money rules under the Corporations Act.

There are two common legal structures:

| Structure | How Assets Are Held | Example Model |

|---|---|---|

| Managed Investment Scheme (MIS) | Pooled unit trust | Common in micro-investing apps |

| Managed Discretionary Account (MDA) | Securities held under your own HIN | Adviser-style robo platforms |

If the platform uses a HIN (Holder Identification Number), your ETFs are registered in your name via CHESS. If it uses a pooled structure, you own units in the fund rather than the underlying ETFs directly.

Important protections and limits:

- Client assets must be held by a licensed custodian or trustee

- Platforms must provide a Product Disclosure Statement (PDS) or Statement of Advice (SOA)

- Robo portfolios are not covered by the Financial Claims Scheme (FCS) because they are investments, not bank deposits

- Capital is exposed to market risk

Platform failure is rare, but market volatility is normal. Safety comes from regulation and structure. Returns are never guaranteed.

Tax implications of robo advisors

Robo advisors do not remove tax obligations. They simplify reporting, but you remain responsible. You may pay tax on:

- Dividends and distributions: These are taxable in the year received. Franking credits from Australian shares may reduce tax payable.

- Capital gains: Selling ETFs or internal rebalancing can trigger CGT events. Gains held longer than 12 months may qualify for the 50% CGT discount for individuals.

- Foreign income and currency exposure: Global ETFs may distribute foreign income, which appears on your annual tax statement.

Some robo platforms offer tax-loss harvesting, which offsets realised gains with losses. This can improve after-tax returns but does not eliminate tax.

Each year, platforms issue a tax statement summarising:

- Dividends

- Capital gains

- Foreign income

- Franking credits

For SMSF investors, reporting integrates into annual compliance processes. If unsure, speak with a registered tax agent.

Who should not use a robo advisor?

Robo advice is efficient. It is not comprehensive. It may not suit:

- Investors with complex tax structures

- High-net-worth individuals requiring estate planning

- Business owners with sophisticated cash-flow needs

- Investors approaching retirement who need drawdown modelling

- Active traders seeking tactical asset allocation

If you require insurance advice, aged care planning, debt structuring or multi-entity tax strategy, a licensed financial adviser provides broader value.

Robo platforms are portfolio tools, not holistic wealth management services.

Who should use a robo advisor?

Robo advisors work well for:

- Long-term investors building wealth over 5+ years

- Professionals who want a hands-off approach

- Investors prone to emotional trading

- SMSF trustees seeking low-cost diversification

- Beginners who want structured ETF exposure

They are particularly useful for investors who would otherwise delay investing or leave cash idle. Automation encourages consistency, and disciplined rebalancing reduces behavioural mistakes.

For straightforward accumulation strategies, robo advice is often sufficient and cost-effective.

How to open a robo advisor account (step-by-step)

Opening an account is usually digital and takes 10 to 20 minutes.

1. Complete risk questionnaire

You answer questions about:

- Income and savings

- Investment time horizon

- Reaction to market declines

- Financial goals

The algorithm assigns you to a risk profile, typically conservative through high growth.

2. Verify identity

Australian AML/CTF laws require identity verification. You may need:

- Driver’s licence or passport

- Residential address

- Tax File Number (optional but recommended)

Verification is usually electronic.

3. Fund account

Transfer funds via:

- Bank transfer

- Direct debit

- Recurring contributions

Minimums vary from $0 to $5,000 depending on provider.

4. Automatic portfolio construction

Once funded:

- ETFs are purchased according to your target allocation

- Dividends are automatically reinvested

- Rebalancing occurs periodically

- You receive online reporting access

From there, the process becomes largely passive. You monitor progress, adjust goals if needed, and let the system manage allocation within your chosen risk framework.

Final verdict: Which robo advisor is best in 2026?

The best robo advisor in Australia in 2026 depends less on branding and more on structure, fees and how much control you want.

If you are starting small, Raiz and Spaceship lower the barrier to entry. Raiz’s round-up investing and $5 minimum make it accessible for beginners, while Spaceship keeps costs simple and app-based. Both prioritise ease of use over deep personalisation.

For true hands-off ETF automation with scale, Stockspot stands out. It is ASIC regulated, manages over $1 billion, and offers disciplined portfolio construction with built-in rebalancing. It suits investors who want structure and behavioural guardrails.

For capped fees on larger balances, InvestSMART is compelling. Its Professionally Managed Account model and fee cap above $200,000 make it attractive for mid-to-high six-figure investors who want active oversight without full adviser costs.

For investors wanting an adviser-style framework with HIN ownership and formal Statements of Advice, QuietGrowth sits in between micro-investing apps and traditional advice.

Ultimately, robo advisors are not about chasing outperformance. They are about disciplined asset allocation, low-to-moderate fees, and removing emotional decision-making. Choose the platform that matches your balance size, complexity and comfort level.

FAQs

Do robo-advisors outperform the S&P 500?

No, robo-advisors typically track diversified global portfolios and are not designed to beat a single index like the S&P 500.

Do millionaires use robo-advisors?

Some millionaires use robo-advisors for low-cost core portfolios, but many also use human advisers for complex planning.

What is the best robo advisor in Australia for beginners?

Beginner investors often prefer low-minimum, app-based platforms like Raiz or Spaceship for ease of entry.

Can you lose money with a robo advisor?

Yes, robo advisors invest in markets, so your portfolio value can fall during market downturns.

Are robo advisors safe in Australia?

Robo advisors operating under an AFSL are regulated by ASIC, but investments are not capital guaranteed.

How much do robo advisors charge in Australia?

Most charge between 0.25% and 0.60% per year, plus underlying ETF fees.

What is the minimum investment for a robo advisor?

Minimums range from $0 to around $5,000 depending on the provider.

Are robo advisors good for superannuation?

Some support SMSFs, but they are not a replacement for comprehensive retirement advice.

Do robo advisors pay dividends?

Yes, dividends from underlying ETFs are typically reinvested automatically.

How are robo advisors taxed in Australia?

Investors pay tax on dividends and capital gains, just like with direct ETF investing.

Are robo advisors better than financial advisors?

They are cheaper and more automated but lack holistic financial planning services.

How long should you stay invested with a robo advisor?

Robo portfolios are generally designed for long-term investing, typically five years or more.